Front-Loading Your 529: Pay tuition with investing gains and avoided taxes, not cash (“superfunding”)

Caitlyn Driehorst is a financial advisor at RightWise Wealth, as well as the firm's founder and CEO. Caitlyn began her career at the Boston Consulting Group and held strategy roles at MGM Resorts, Capital Group American Funds and two venture-backed wealth startups. She holds a B.A. from the University of Chicago and an M.B.A. from UC Berkeley's Haas School of Business.

Published: July 24, 2025

Updated: April 23, 2026

This is my magnum opus: the single, surprising thing I’d most-want well-paid, good-hearted people in their 30s to understand, to benefit their eventual interests.

This post is long, but could easily be longer. (Want the results but not the scrolling? Reach out to chat with one of the advisors at my firm. We can bring this rigor not only to your education goals but also to your budget, retirement, insurance coverage and end-of-life planning.)

There’s two potential buckets of funding for your child’s college tuition: there’s cash, and then there’s investment gains and tax savings. A lump-sum funding strategy optimizes for the latter, and the dollars associated with its success may shock you:

This is truly what they mean when they say, “it’s cheaper to be rich than it is to be poor.”

First, we’ll review three things you should understand when thinking about your 529 savings strategy:

However expensive you think college is or will be, it’s probably more expensive

The tax benefit on 529 plans is entirely on the investment gains

The value of compounding increases significantly with time

Then, you’ll see how these come together into the idea that you should front-load lump-sum your 529: fund the account as early as reasonable, and as big as makes sense for you. “Two blue lines on a stick” early, even. “Supplementing folic acid,” early. It’s called “superfunding,” folks.

Please see important disclaimers, nuances and notes on methodology at the end of this article. It’s not just boilerplate: investing always includes the risk of loss, including loss of principal.

All of our writing on this topic is now available as a book! Complimentary copies upon request.

Part One: Three Things to Understand

My son, Jonny: “Like a tree, he’ll grow, with his head held high, and his feet planted firm on the ground…”

Attending college is stupid, stupid expensive

I only applied to two colleges, and I got into both:

University of Maryland, College Park, offered me a bonkers scholarship: not only acceptance, not only a full ride, not only preferred enrollment for classes, not only study abroad on-the-house, but I’d get a small cash stipend. They’d pay me to attend.

The University of Chicago said they’d let me in — and how convenient, my cute little National Merit Finalist money would reduce my need-based aid.

I remember sitting on a park bench with my dad and pleading dramatically, as a 17-year-old does: “My whole life, I’ve been the weirdo. UChicago is my first chance to feel normal.” My parents – both public servants at the time – made huge sacrifices so I could attend this school. “You know, people at church thought we were crazy,” my mom has since let me know. (Mom and Dad, I know you read everything I write — thank you, I love you.)

Four years later, when I got my job offer from the Boston Consulting Group, my parents were shocked by my starting salary. That first job has been the bedrock of my whole career – and UMD definitely wasn’t a “target school” for BCG recruiting. In the road not traveled, I would have had less debt – and a shallower career trajectory.

Look, I don’t like it; but it’s true.

That comes at a price, and the price has risen probably faster than you realize:

The total estimated cost for four years, if my little son, Jonny, attends U of C in 2042? Around $940,000 in future-dollars.

What it looks like setting up a college goal in our financial planning software — this isn’t Jonny’s real account!

There’s “scary” and then there’s “scarier”: as the federal government pulls back funding, tuition may increase even more rapidly than current projections based on pre-Trump trajectories.

Of course, UChicago is ritzy: there’s gargoyles and students are placed into houses, like in “Harry Potter.” Attending a public university is about a third of the cost of such a private university. Right Capital’s estimate for four years of non-profit in-state average all-in cost of attendance in 2042 is much lower, at “only” $295,477.

Think about going into your bank account and making a semester-sized payment to cover that amount, each payment enough to buy a car. Eight semesters, enough to buy eight cars. Think about typing in the first digit and then hitting zero-zero-zero-zero and watching the comma move. Let that sink in.

Takeaway #1: However expensive you think sending your child to college will be, it will probably be more.

The tax benefit for a 529 is entirely on the investment gains

Most people are familiar with the tax benefits of a 401(k): you save out of your paycheck, that money isn’t taxed today, and then when you pull out the money in retirement, you’ll owe income taxes. Today, tax break; later, pay taxes.

A 529, by contrast, works like a Roth IRA. The money you contribute comes out of your take-home paycheck; you’ve already paid income taxes on it. There is no immediate tax benefit to contributing to a 529. But, when you go to pull out the money for qualified reasons, you won’t owe any taxes on the investment gains. Today, pay taxes; later, tax break. (Note: some states offer a pre-tax benefit for residents investing in their state’s plan.) (Read the official IRS documentation here.)

How this works: Suppose you invested $50,000, and fifteen years later, that investment is now worth $100,000. If you’d invested in a general investing account, you’d owe taxes on the $50,000 of gain in the account. But if that investment were in a 529 account, and the withdrawal applied against a qualifying educational expense, your tax bill would be nada.

Takeaway #2: If you want to maximize the tax benefits of a 529, you want to maximize the investment gains in the account.

The value of compounding increases significantly with time

When I was at Capital Group American Funds, our archive had brochures from the 1950s showing versions of this classic anecdote, illustrated here by the St Louis Federal Reserve.

It’s a classic for a reason: the effects of compounding are so much more powerful than your intuition may suggest. This is why we say, “first, you work for your money; then, your money works for you.”

Investing less, for longer, can result in greater outcomes than investing more, but starting later.

Takeaway #3: To maximize the investment gains of an account, start investing as early as possible.

Part Two: How Does This Come Together?

So we have shown:

The cost of college education is bonkers

To maximize the tax benefit of a 529, you want to maximize the investment gains

To maximize the investment gains in an account, you want to start as early as possible

Combined, these three factors suggest that lump-sum funding your 529 as early as possible can maximize the extent to which your child’s tuition is paid for by investment gains and tax savings, rather than earned and saved cash.

Let’s show how this strategy would work in practice, and contrast it with a traditional savings strategy:

Percy the Example Child was born on July 15, 2025, and he will be starting college in 2043; his parents have set the goal to cover 100% of in-state public tuition, and he can borrow above that if he decides to go to a private school.

We’ll use Right Capital’s projection tools to compare two funding strategies for his parents to reach this goal. (Want us to use these same tools to help you and your spouse understand various funding strategies for your children? Reach out for a discovery call with our firm.)

Strategy #1: What if Percy’s parents fund $80,000 into his account the year he is born, then never save again?

In this projection, you can see how the investment returns are added to the original balance of Percy’s account, so his parents start earning investment returns on top of the investment returns. That’s compounding, folks.

See “Notes and Nuances” below for assumptions and methodology

When Percy the Example Child starts college in 2043, his 529 has $256,424 in the account – that’s $176,434 of investment gains, and his parents don’t owe a dime of taxes on that increase, because of the 529 wrapper. (Otherwise, they’d owe around $35,284 in taxes on those gains, assuming 20% capital gains bracket. Who around here feels like not paying $35,000 in taxes? 🙋!)

Right Capital tells us that with this investment, Percy’s tuition would be 98% covered.

Strategy #2: What if Percy’s parents wait until he’s five, and then save $12,000 each year until he is 18?

Hey, big kudos to Percy’s parents!! That’s a lot of saving. That’s $1,000 every month from kindergarten through the end of high school. We often hear parents suggest this strategy because it’s timed with their child starting school and no longer having to pay for full-time childcare. Especially for those in high cost-of-living areas, that intuition is especially sympathetic.

Here’s what that account balance looks like in Right Capital:

The good news: Right Capital tells us that with this strategy, 97% of Percy’s public in-state college costs will be covered by this 529 balance. Very similar outcome to the first strategy! And congrats to Percy’s parents for making that happen.

But here’s the thing: these two strategies both took Percy’s account to similar outcome, but Strategy #1 is sending him to college mostly with investment gains and tax savings. Strategy #2 is mostly sending him to college with mostly cash:

What’s crazy is that Strategy #2 — starting later and spreading your savings over time — feels cheaper, but it actually more than twice as expensive, going by total cash required to achieve the similar outcomes by freshman year.

Again, this is what they mean when they say, “it’s cheaper to be rich than it is to be poor.”

There’s tremendous privilege in any strategy that starts with, “suppose you’ve got $80,000 hanging around.” But many of us are in that fortunate position. Reflecting on the big picture, I agree with Ron Lieber’s opinion from his excellent 529 overview in the New York Times: if you’re taking advantage of a five-figure tax forgiveness for your children’s education, then you have a moral obligation to support subsidies and student loan forgiveness for the children of other parents with less fortune and less access.

So let’s say your child was born in 2026, and will be starting college in 2044, and you want to lump sum their entire future cost of tuition in a 529 in the year they’re born. Approximately how much would you want to lump-sum today to cover projected average costs of full attendance?

It may not be realistic – or the best use of funds, relative to other goals! – for you to put that full lump sum down at once, that early.

However, something is better than nothing, and now is better than later.

529 Superfunding: How can you implement this strategy without triggering gift tax? Read Part II.

Thank you for enduring and engaging with my soapbox. I am so passionate about this topic and this recommendation.

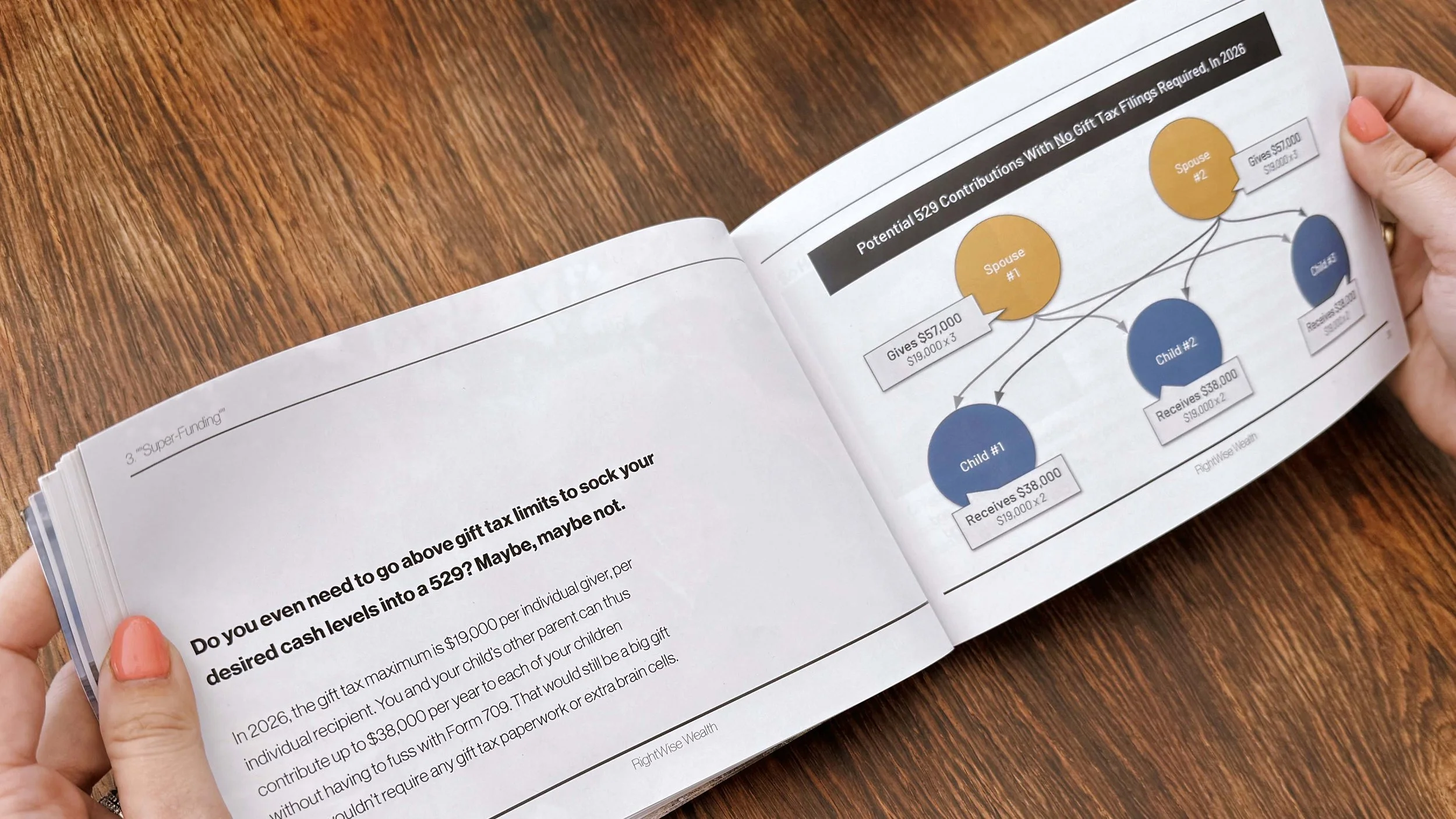

“But Caitlyn,” you ask me. “Thanks for the ‘why’, but what about the ‘how’? The Internet says that the most I can contribute to a 529 in 2026 is $19,000 without gift tax implications. How can I lump-sum fund my child’s 529 to the amounts you’re describing?”

Call it “one weird trick” – there are strategies that don’t trigger gift tax concerns, including the strategy my husband and I are using for our son.

You can also request a complimentary copy of our book, “Front-Load Your 529,” to learn more about superfunding

Want to work with someone who can do the math for you?

This may be the first time you’re learning how 529 accounts work. But this is something we work with all the time on behalf of our clients. You absolutely could research plans, download the PDF disclaimers, figure out the underlying fund menus — or you could throw it over the fence to someone who loves this stuff.

We’d love to talk with you about the long-term, holistic financial advice relationships we build with our clients. Book a discovery call below.

Notes and Nuances:

You know what also benefits from front-loading and years of compounding? Your retirement. This strategy assumes you are in a good place for your retirement; if you’re not, then that should take priority over funding your child’s education. As the saying goes, “student loans exist, but there’s no such thing as a retirement loan.” Our financial advisors can use software to help you make these decisions based on numbers, not vibes.

In real life, we don’t always advise that 529 is the only source of coverage for college tuition. You may want to complement 529 savings with a flexible taxable brokerage account or cash savings (especially if college is sooner rather than later), and we can also assume that your student may borrow a certain amount each year.

If you live in a state whose plan has a state income tax benefit, some level of annual contribution may make sense for you

A lump-sum contribution risks poor market-timing on a short-term basis. I wouldn’t over-think this, given a >15-year time horizon, but you could dollar-cost average by investing chunks over time if you were concerned

All projections assume that 529 contributions are invested in an aggressive 100% equities portfolio through their whole lifecycle; this may or may not be how your 529 would be invested. These projections are intended as general educational illustrations and are not a promise of returns.

Investing always includes the risk of loss. We assume all years have similar performance of compounding 7.1% returns, for simplicity, but in real life, some years are better than others, and some could even be negative. “What if the market took a nosedive Fall of their freshman year?” is a fantastic financial planning question.

We’re assuming no fee drag on accounts, for simplicity. Some states’ 529 plans have surprising fees, and sometimes those fees are hard to figure out. (Looking at you, Nevada’s JPMorgan 529. They advertise a $300 kickstart bonus for low-income families and then on page 5 and page 6 of the PDF linked in the small-print, you see some gobsmacking fees. I just helped my sister side-step this one.)

RightCapital's college national average costs are from CollegeBoard.org published data, while specific college costs are taken from published Department of Education data.