Tax Alpha Decay: Why You May Not Be Getting Tax Loss Harvesting With Market Volatility

On March 20, 2026, the S&P 500 was down 9% from highs just a few weeks earlier. Some of our clients were getting tax loss harvesting opportunities left and right – and others, not.

Why is that, when they’re largely invested in similar funds? If you’re hoping for more tax loss harvesting opportunities, what strategies should you consider? Read on!

Caitlyn Driehorst is a financial advisor at RightWise Wealth, as well as the firm's founder and CEO. Caitlyn began her career at the Boston Consulting Group and held strategy roles at MGM Resorts, Capital Group American Funds and two venture-backed wealth startups. She holds a B.A. from the University of Chicago and an M.B.A. from UC Berkeley's Haas School of Business.

Published: April 2026

First, what is tax loss harvesting and why do we love it for our high-earning clients?

Our clients are commonly in the highest-earning years / decade of their careers and they often have state burdens from living in California, New York or Washington, DC; to the extent that we can shift their tax burden from these crazy years towards later in life, we do so with glee.

“Tax loss harvesting” is one of our favorite tools, which builds on the following facts:

At the end of the year, you’re taxed on your NET investment gain. You probably just assembled all your 1099s; your software or tax professional uses these to add up how much you made and how much you lost while investing in a year. Losses are powerful because they can offset gains, such that those gains are “free” from a tax perspective.

You’re only taxed on your REALIZED gains and losses, not paper gains or paper losses. You know how you have some stocks that are way up since you bought them, but you haven’t owed any taxes on that? Gains don’t count towards that net figure until you sell the stock. And… losses are the same way. If you’ve lost on paper, it’s not “real” for your net calculation at the end of the year

Recoveries tend to be sharp and staggered, not low slow grinds back up, so you want to stay invested rather than staying in cash and seeing how that goes. But, you can’t hop back into the position you just exited and still claim it as a loss – this is a “wash sale,” which has even more nuance – a topic for another day.

So to reduce your investing taxes today, you want to realize losses while staying invested (and avoiding wash sales.) How?

You have a loss in your portfolio: You bought a stock for $15 and now it’s worth $12.

SELL! You realize that loss with a sale. You’ve now lost $3, which will count against your net gain at the end of the year.

INVEST! You hop that money over into something similar but different enough for IRS purposes. You take that $12, shimmy it over into something similar but different, and wait for the market to rise back up.

Implicit in tax loss harvesting? You need losses. And depending on how much your portfolio has gone up since you funded it, even bigger drops like recent volatility from the war in Iran may not get you there.

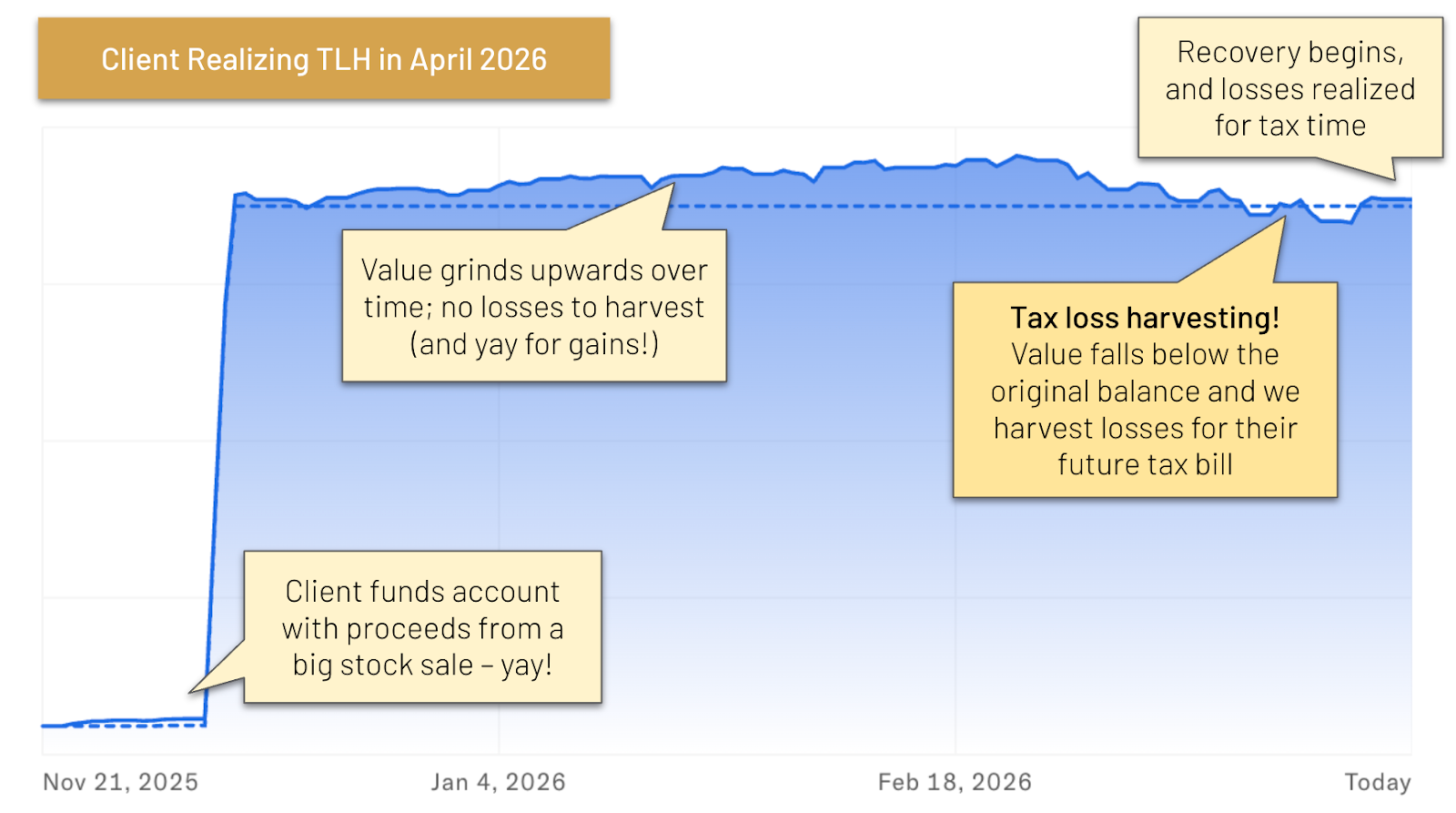

Here’s an anonymized example of a real RightWise client portfolio, which has seen some nice little tax loss harvesting opportunities over recent weeks:

You can see that this account was mostly funded by a lump-sum deposit late last year, after a big stock sale. Though the value has grown some in the intervening months, the recent volatility has brought the total value of their portfolio below their original investment, generating opportunities for tax loss harvesting.

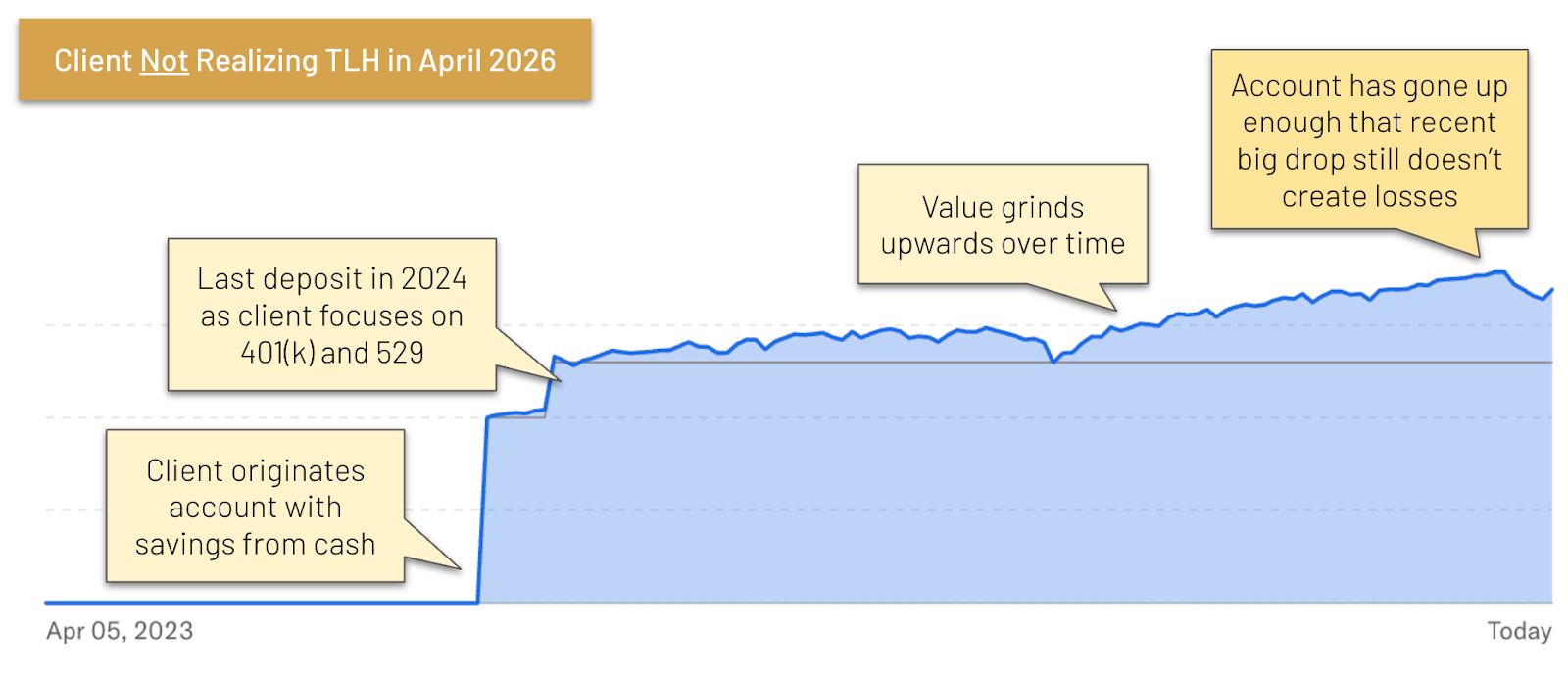

That’s not every account’s story. Here’s an example of a client’s taxable account in which there have been no recent TLH opportunities. The account was last funded in 2024 – this client is a fantastic saver, just focused on other accounts! – and it’s appreciated enough that even recent drops still leave them with plenty of gains on paper. So, no TLH opportunity… but also, no tears! Yay for this client’s account going up. It would be a bummer if they’d been invested for two years and in a net loss.

So in general, we see:

Newer money = higher cost basis

Higher cost basis = greater probability for near-term net loss, given normal market volatility

Greater probability of loss = greater opportunities for tax loss harvesting

This phenomenon – that tax loss harvesting opportunities tend to fade over time, as portfolios appreciate – is called “tax alpha decay.” Very sexy name. Here’s how the name breaks down:

“Alpha” refers to investment return attributed to manager skill or action rather than attributed to the market going up just generally

“Tax alpha,” then, is specifically returns attributable to tax moves

“Tax alpha decay” describes how opportunities for tax alpha tend to be less common over time

So if you have an account with tax loss harvesting turned on, or an advisor overseeing this for you, and you aren’t seeing any tax loss harvesting results, this is probably why: the value of your investment has risen over time (yay!) such that even these recent big dips aren’t creating loss opportunities.

So what can you do? What strategies can help you extend the life of tax alpha opportunities in your portfolio? What is the retinol cream of tax alpha decay?

Strategy #1: “Dollar cost averaging”

DCA: it’s not just the best airport for flying into our nation’s capital. Dollar-cost averaging refers to making regular deposits into an investment account, “averaging” out the dollars you’re investing over time (and over a range of stock prices.)

You probably already dollar-cost average into an investment account: this is how most 401(k) savers contribute to their retirement accounts. (Note, of course, that there’s no tax loss harvesting in 401(k) accounts since there are no taxes inside those accounts.) Every two weeks, a set dollar amount is withdrawn from your paycheck and put into the account.

This can also be a useful strategy for your taxable account.

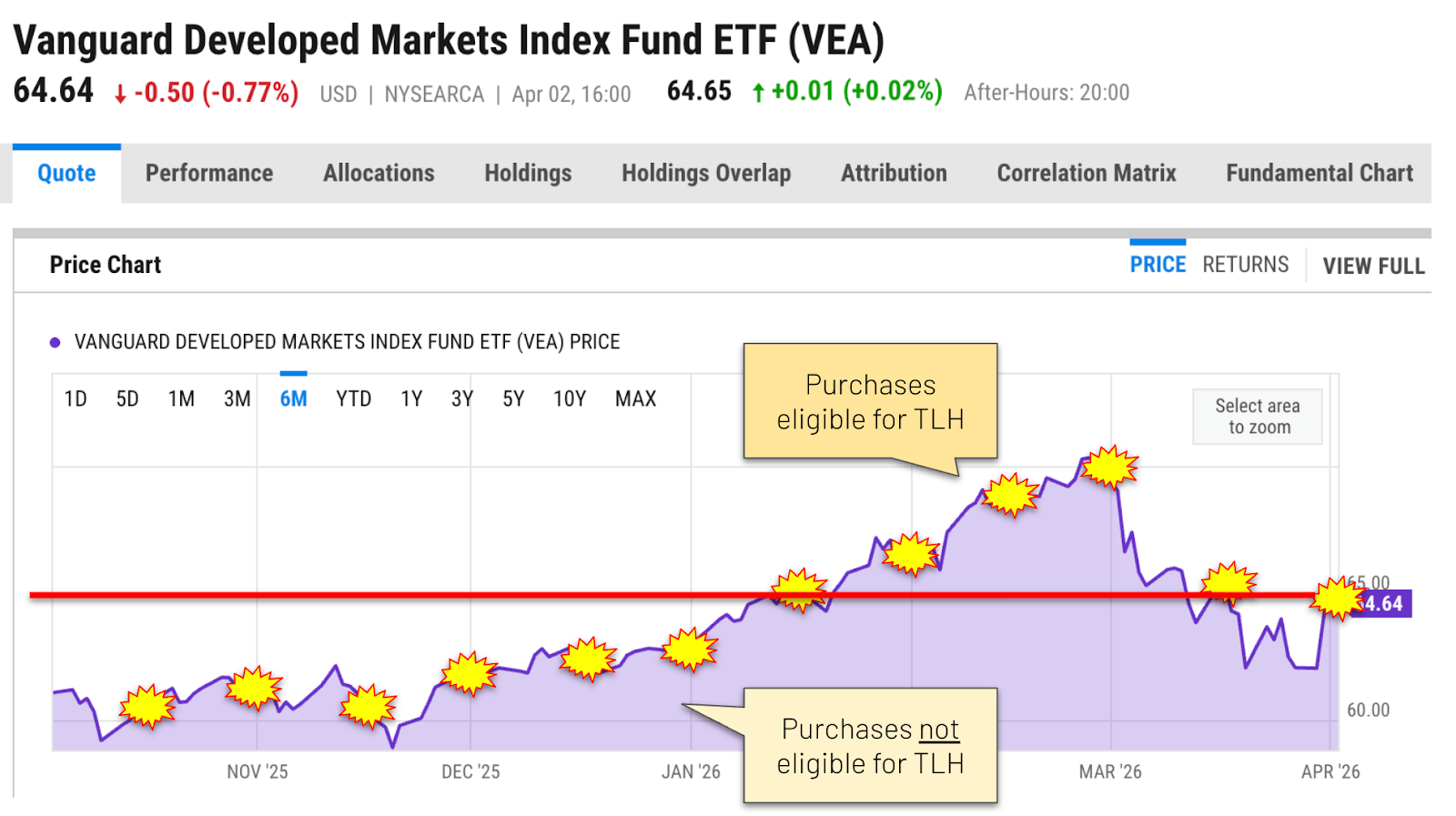

Consider the below example of someone who is dollar-cost averaging every two weeks into VEA, an ETF for international developed markets equities. Because their purchases (little yellow explosions, you’re welcome) are spread out over multiple dates at multiple prices, some will be in gain and others will be in loss, potentially creating more opportunities for tax loss harvesting.

When clients are investing lump sums for the long term, we usually don’t advise dollar cost averaging: as Harry told Sally, “when you know you want to spend the rest of your life with someone, you want the rest of your life to start as soon as possible.” Time in the market – and long-term gain – is our priority for those one-time large amounts.

And where clients have other investment priorities – cash for a down payment, two partners both maxing 401(k), front-loading a 529 – their taxable brokerage account may not be the household’s first priority for ongoing contribution. (Now that I’m a mom, I feel more empathy for the poor 401(k) – we do so much for so many people, yet so taken for granted! Mothers Day is May 10, guys, heads up here.)

But where a client is dollar-cost averaging into taxable, our head swings on a swivel point towards tax loss harvesting opportunities, since that “fresh powder” is so desirable for this strategy.

And where that DCA is a priority, and we want to maximize TLH – that brings us to our second strategy for maximizing tax loss harvesting opportunities: direct indexing.

Strategy #2: “Direct indexing”

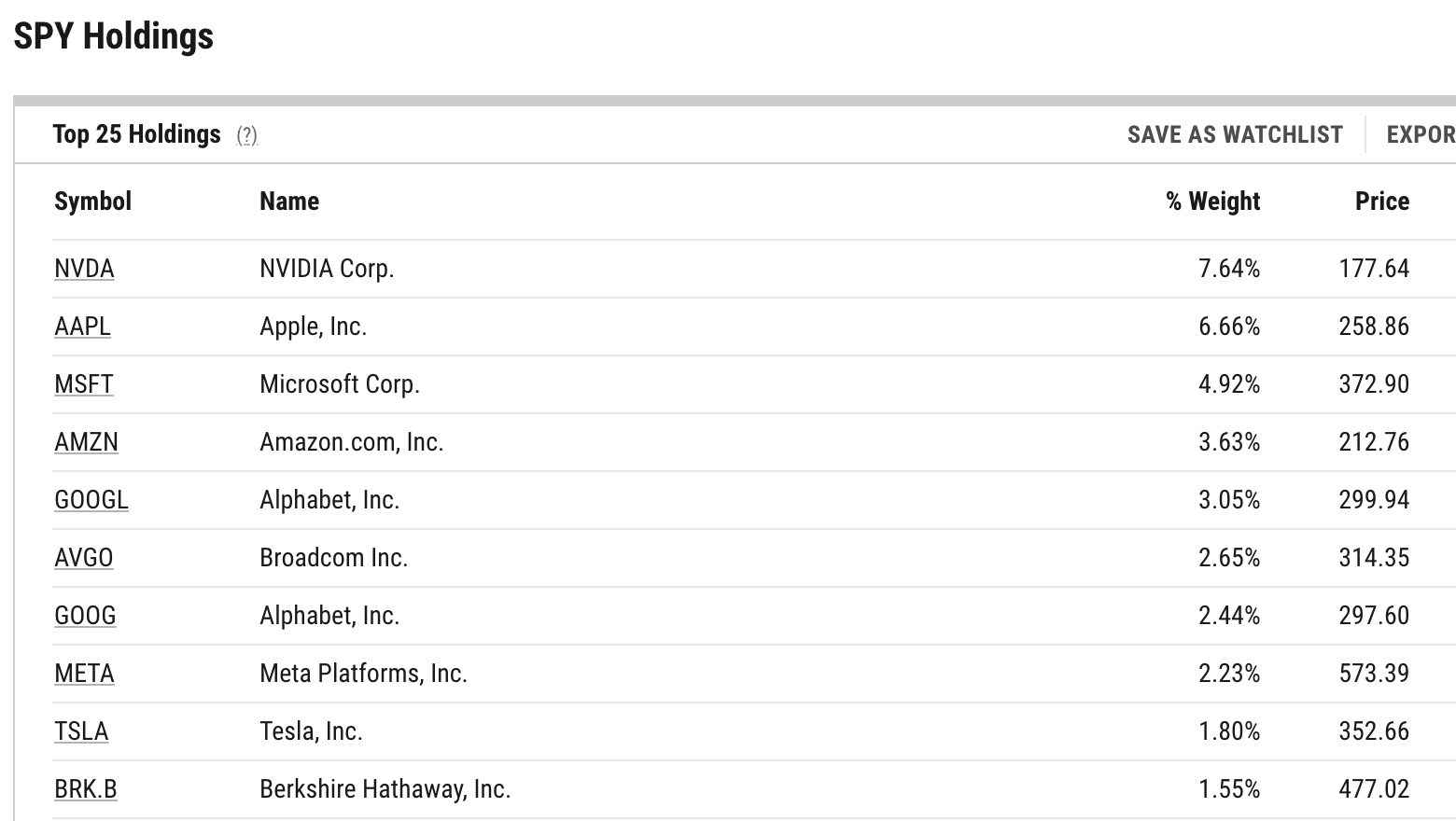

I love talking to clients about what they hold in their portfolios; one “magic trick” is pulling up an ETF to show them the underlying holdings. For example, here’s the holdings for SPY, the famous S&P 500 ETF, as of April 6, 2026:

When you buy an ETF, you’re buying all of these underlying companies. With one neat clean Marie Kondo-approved ticker, you get all of these holdings. Easy, cheap, simple diversification.

One reason we love diversification is that it “smooths your ride” – rather than the craggy roller coaster of a concentrated holding in a single stock, your portfolio reflects the aggregate performance of a total index.

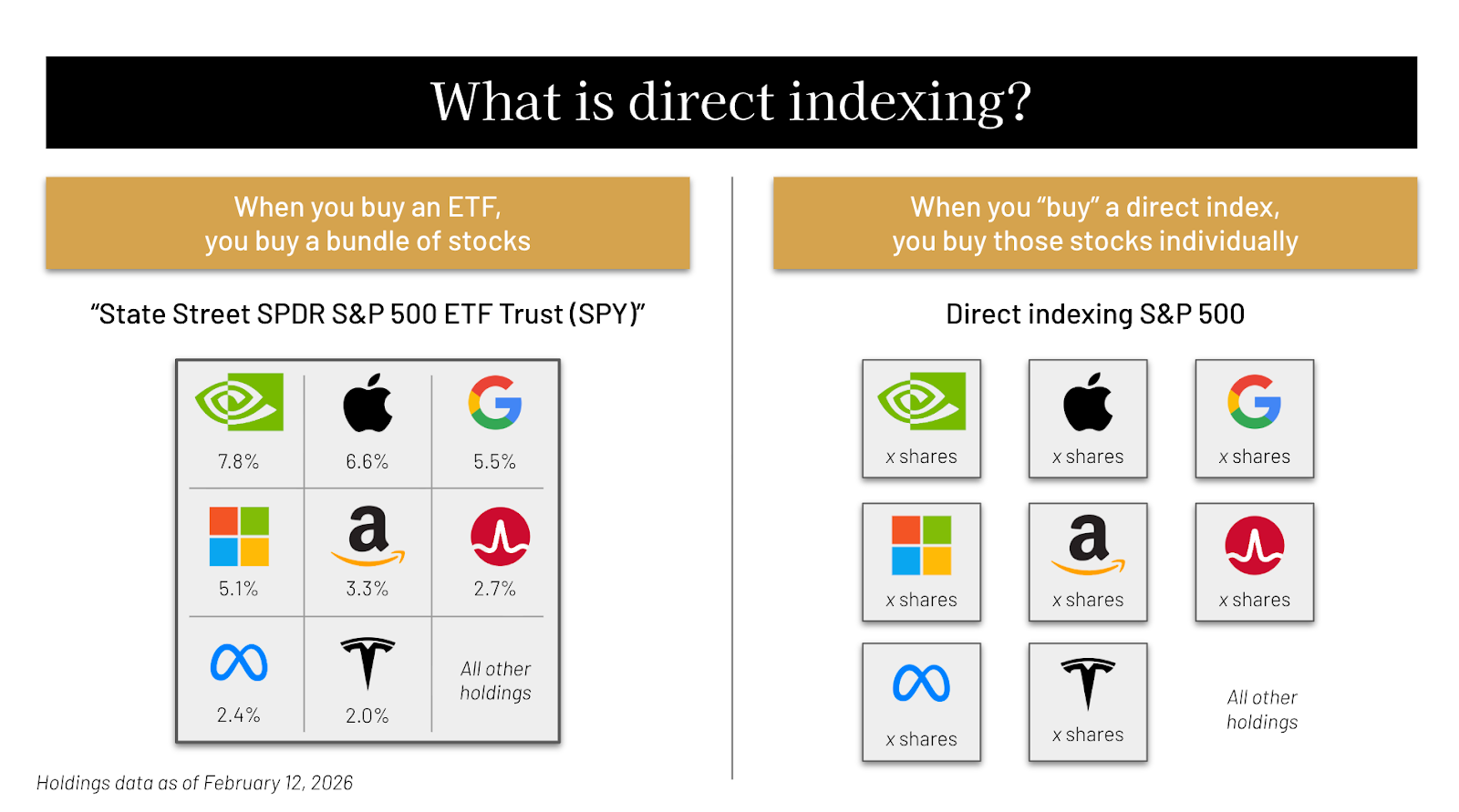

But what if you want some churning waters? You’re in a very high tax bracket, deferred taxes have great value to you, you want more opportunities for tax loss harvesting while still being diversified. My friend, meet direct indexing:

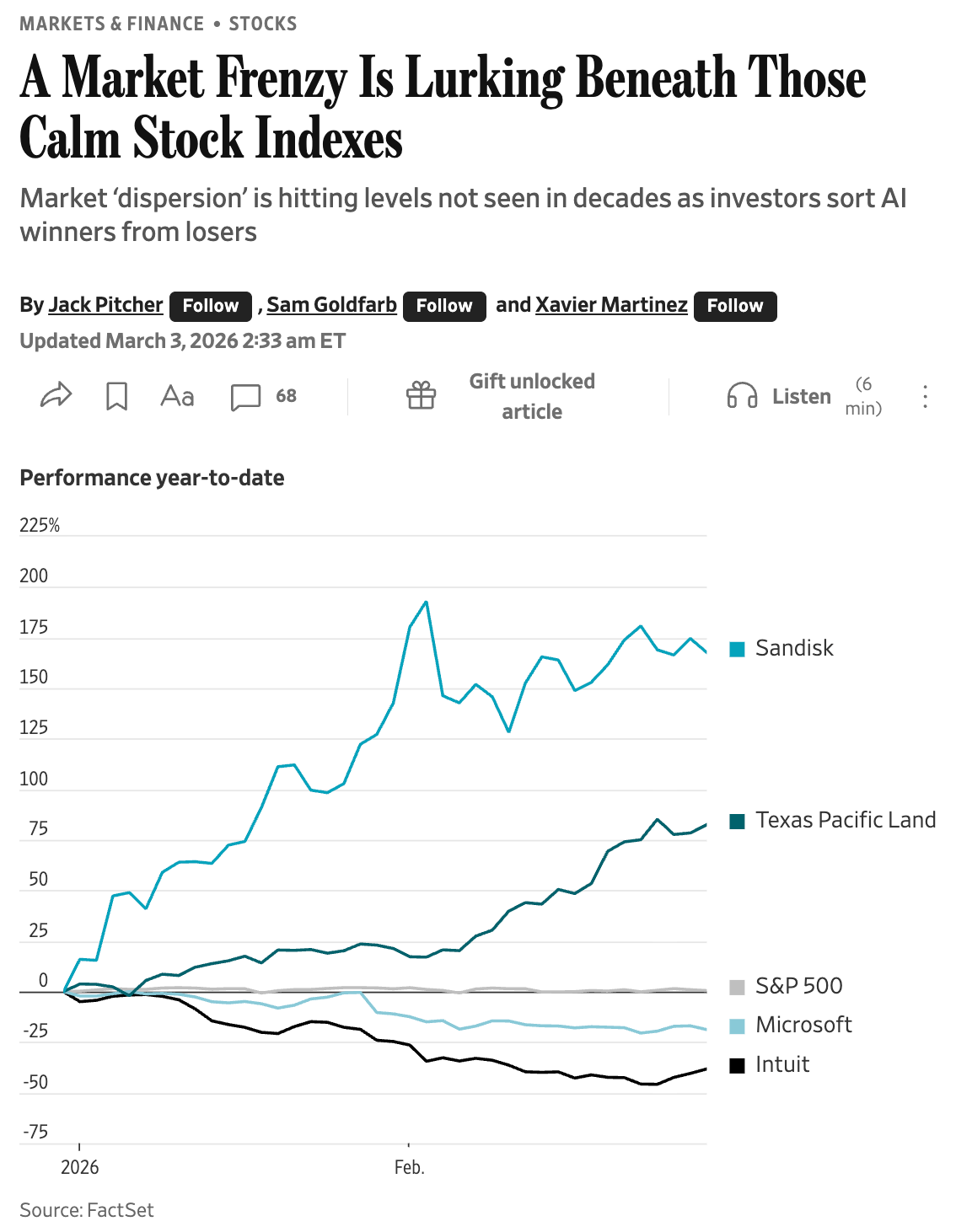

Rather than own a single ETF, you own the underlying positions – and all their underlying volatility, which these days, is considerably more than the volatility of their index:

In the above example, the S&P 500 is pretty flat – but Microsoft and Intuit are down over that same time period. Where the index wouldn’t give you a TLH opportunity, those individual positions may.

This is how direct indexing can create a larger number of tax loss harvesting than holding similar investments within ETFs.

Tax loss harvesting can be amazing, but as we’ve shown, these opportunities “decay” over time. And if you go with a strategy like direct indexing, you’re left with a complex portfolio of many positions, requiring careful rebalancing and likely some degree of indefinite professional management. When is that complexity worth it?

I asked John Hill, co-founder at Quorus and former head of direct indexing at Vanguard, for his take. (RightWise is a happy Quorus customer!)

“Tax alpha decay is real. Eventually, you’ll end up with all your lots in some degree of gain. That’s not a bad thing; that’s successful investing. And even with that sort of ‘dead portfolio’, you have tax strategies that you can play with: donating your most-appreciated shares to a donor-advised fund, for example.

“As for the ongoing complexity, today, the logistics of direct indexing are mostly automated: no one is hand-transcribing 1099s into your annual return. So any aversion to complexity is mostly psychological, but psychology is real, maybe especially in investing.

“This is why I think direct indexing is a tool for financial advisors, not a panacea for every person’s portfolio. You need to do the math on the value of deferred taxes, and understand whether the value merits the complexity, fees, etc. I won’t sit here and say that math pencils for every investor always.

“But for high-earning clients, that math can be pretty definitive. One of the foundational insights of investing is that a dollar today is worth more than a dollar tomorrow: a dollar today can grow with years of compounding, whereas the purchasing power of a dollar in the future is diluted by inflation.

“And deferring taxes from a year in which you’re in a 55% marginal tax bracket to a future year where you’re traveling the globe in early retirement with plenty of room in your 0% capital gains bracket — that can be pretty magical stuff.”

If you are in the highest-earning years of your career, you are in the highest-tax years of your life — and those years deserve a proactive strategy, not an April retrospective that leaves you wondering what exactly happened (and maybe what should have happened.)

We take pride not only in offering tax filing via an integrated partnership, but also in holistic financial planning that pulls together all the dollar signs in your life into one picture.

We’d love to hear about your life; request time with an advisor via the button below.