The 30-Second Chore Standing Between Your Ex and Your 401(k): Account Beneficiaries 101

Credit: The Wall Street Journal

I call them “yuppie campfire horror stories” — the woman whose asset-backed mortgage got margin-called when her employer stock tanked, the TTC mother-to-be who didn’t realize declining short-term disability during open enrollment would set her maternity leave sideways.

The Wall Street Journal comes through with one such tale: a man’s million-dollar 401(k) is left to his ex-girlfriend, as he’d scribbled her name on paperwork decades earlier when he started his new job, and never updated the paperwork. Oops?

Account beneficiary designations are a pesky chore, but they bypass your will, and it’s worth the time to get them right. Read on for 101 that somehow never made it your way during high school.

Caitlyn Driehorst is a financial advisor at RightWise Wealth, as well as the firm's founder and CEO. Caitlyn began her career at the Boston Consulting Group and held strategy roles at MGM Resorts, Capital Group American Funds and two venture-backed wealth startups. She holds a B.A. from the University of Chicago and an M.B.A. from UC Berkeley's Haas School of Business.

Published: May 2025

Why Account Beneficiary Designations Matter

Here’s how it goes when assets are directed by your will:

Your will is filed with the courts

Your family waits – weeks in some states, months or years in others

The court approves the directions provided by your will in a publicly-available set of proceedings

The court and attorneys charge your estate a percent of its value as compensation for its time.

Here’s how it goes when assets are directed by an account beneficiary designation:

The named person calls the institution, provides the required paperwork

The account transfers over

That’s it, that’s the end of the steps. No wait, no judge approving things, no fee, no public documents.

This is such a magical hack to meet both your “control” and “convenience” goals for estate planning!!! … provided, of course, that your listed beneficiary is still who you want to get those assets.

If your wishes have changed, that easy transfer can direct your money according to outdated plans… more on that in a minute.

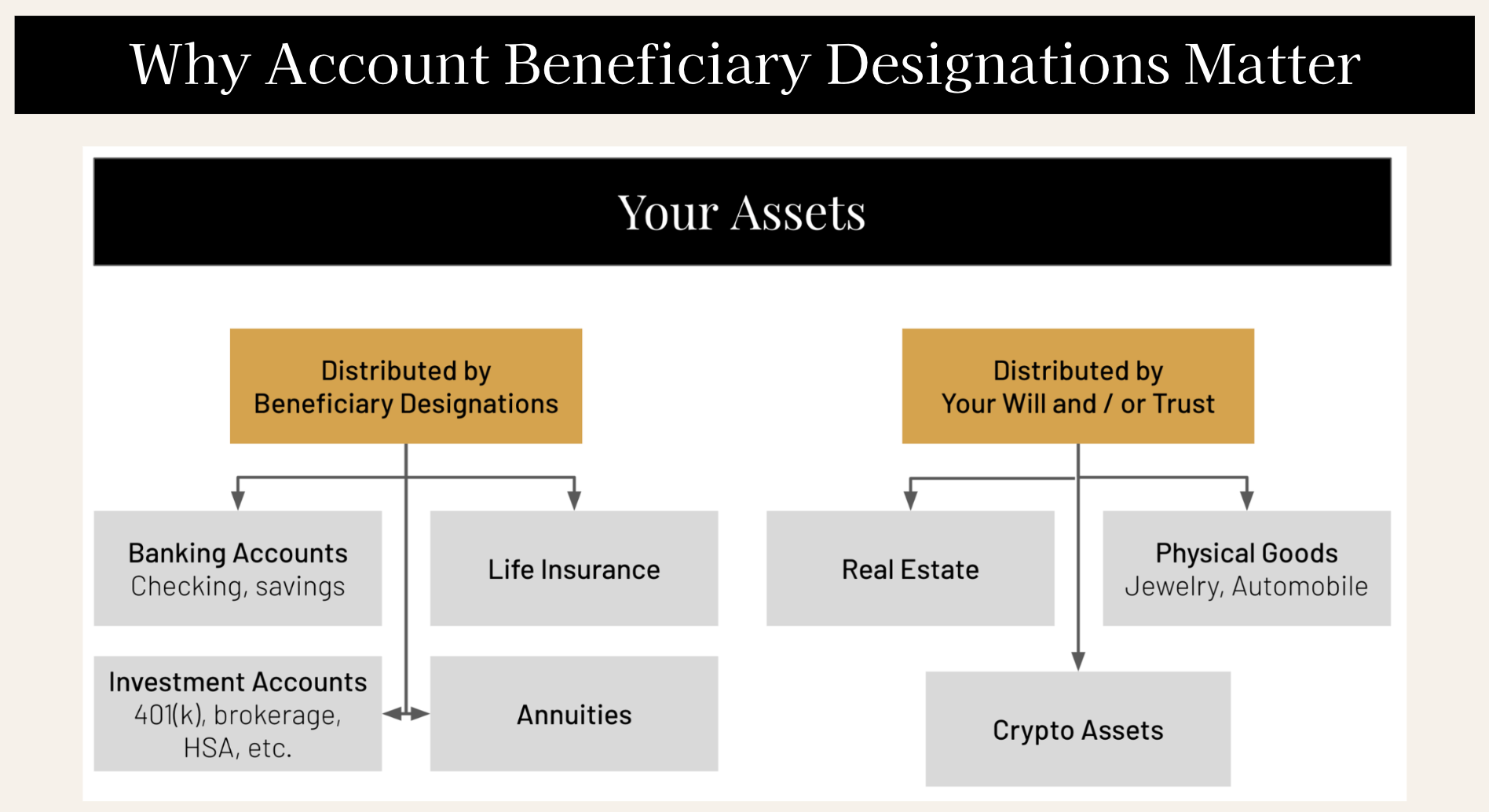

Which Accounts Are Directed by Account Beneficiary Designations?

“If it’s money, it’s directed by account beneficiary designations; if it’s stuff, it’s directed by your will” is a useful rule of thumb.

Special call out for crypto accounts! You may think of these as financial assets, but they are directed by your will, not account beneficiary designations.

If you have crypto assets, make sure they’re addressed in your will and that you’ve left instructions such that your assets can be recovered by a loved one who may not be as tech savvy as you.

Whom Can You Name as a Beneficiary?

When most people imagine a beneficiary, they think of a person — but it doesn’t have to be.

The first (and generally most popular) option is to name a natural person. It’s pretty straightforward: make sure you’re using their full legal name and get the spelling correct. You should also make sure that they know (or will know) to contact the institution and claim those assets, should something happen to you. Some institutions will let you add a Social Security Number, birthdate, and contact person, as well as the name.

A second option is listing a non-profit. Planned giving can be a great way to support your favorite causes. Make sure to use the organization’s legal name and provide a Tax Identification Number if you can. If you call the organization you want to donate to directly, they will probably be more than happy to help you.

Finally, you can also opt for assets to flow to your estate instead of listing an account beneficiary. That means that your assets wouldn’t go straight from the account to one particular person, but instead they’d join the rest of your estate and be distributed according to your will. The catch is you need to actually have a will written (and up to date!) so your assets don’t get tied up in court or distributed in ways you no longer want.

You can also list a trust as an account beneficiary — here, you may want some professional guidance. (Related reading: our post, “Should Your Parents’ House Be In A Trust?”)

Special Considerations When You’re Married

If you’re married, “the system” assumes you’ll want to transfer assets to your spouse. For many married couples, this fits just fine. There’s a degree of privilege in having some favorable tax treatment and having default conditions anticipate your preferred beneficiary. Also, a spouse has options, like rolling an IRA into their own IRA or keeping the tax advantages of an HSA, that other beneficiaries don’t.

If you have a joint banking account with your spouse, these accounts are commonly set up as “joint accounts with rights of survivorship,” meaning your spouse will automatically assume the account if you pass away. The two of you may still want to choose a beneficiary who’d inherit the account in case you are both in the same unfortunate car accident, etc.

Going against the grain can be tricky. If you want to leave a workplace retirement account (e.g., 401(k)) to anyone other than your spouse, you may need a lawyer to help with papers. Alternatively, you can roll over assets into a Traditional IRA, which doesn’t have the same spousal protections.

Finally, if you have a prenup, make sure your designations are consistent with that commitment, or otherwise documented. You don’t want two documents at cross purposes.

(Are you a parent who isn’t married? Some thoughts for you in our blog post, “Financial Moves for Mothers Who Aren’t Married.”)

We Help Our Clients Conquer Pesky Chores

Yes, there’s a good piece of strategy, but most of good estate planning is chores. It’s keeping your account beneficiaries up-to-date, retitling your accounts, finding the settings in your Instagram account so someone could shut down your account if necessary. Nothing like existential reckoning mixed with lots and lots of paperwork.

When you work with a financial advisor like RightWise Wealth, we streamline this process with trackers and check-ins. Always available to answer questions, our advisors are your whole-financial-life chore buddy.

(Also, our financial planning fee includes end-of-life documents, including wills, trusts, etc. Since you’re already paying for it, you’re one step closer to completing these!)